By Prasenjit Gupta, Founder, Clover Capital | Wealth Management & Financial Services, Kolkata.

AMFI-registered Mutual Fund Distributor | 55+ man-years of combined advisory experience | Last Updated: June 2026

What You’ll Learn in This Guide

Whether you’re a first-generation investor or someone with a few years of market experience, this guide answers the questions we hear most often at Clover Capital:

- What does portfolio rebalancing actually mean?

- How do I know when my portfolio needs rebalancing?

- What is the right rebalancing strategy for my risk profile?

- How often should I review my investment allocation?

These are informational questions with real financial consequences — and the answers matter more than most investors realise.

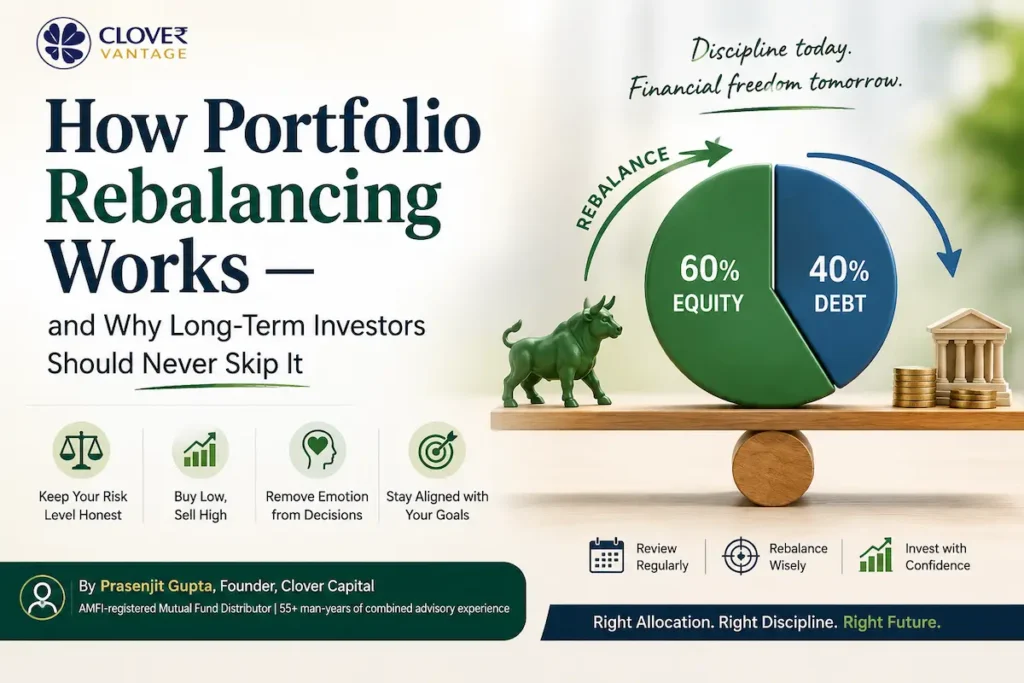

What Is Portfolio Rebalancing?

Portfolio rebalancing is the process of restoring your investment portfolio to its original target allocation after market movements have shifted the proportions.

When you invest, you choose a mix — say, 60% equity mutual funds and 40% debt instruments — based on your financial goals, investment horizon, and risk tolerance. Over time, markets move. Equities may outperform and grow to 72% of your portfolio. Your original 60-40 plan has silently become something riskier and different — without you making a single active decision.

Rebalancing corrects this drift. You sell a portion of what has grown disproportionately and use those proceeds to buy what has fallen behind, restoring your intended allocation.

In short: Rebalancing is not a market-timing strategy. It is a discipline that keeps your portfolio aligned with who you are as an investor — not who the market wants you to be.

Why Experienced Financial Advisers Recommend Regular Portfolio Reviews

1. It Keeps Your Risk Level Honest

Every investor has a risk profile — conservative, moderate, or aggressive. Your original asset allocation reflects this. But asset drift quietly changes your risk exposure without any action on your part.

A conservative investor who set a 50% equity allocation in early 2023 may have seen that figure climb to 65% or higher by 2025 due to strong equity market returns. That investor is now bearing more risk than they originally chose to accept.

Rebalancing is the corrective mechanism that keeps your risk exposure honest.

2. It Enforces Disciplined “Buy Low, Sell High” Behaviour

One of the most well-established principles in long-term investing is buying undervalued assets and trimming overvalued ones. Yet behavioural finance research consistently shows that individual investors do the opposite — they hold winners too long and avoid buying beaten-down assets.

Systematic rebalancing counters this bias. When you sell a portion of your outperforming equity funds to top up your underperforming debt allocation, you are mechanically selling high and buying low — without relying on market predictions or emotional judgement.

3. It Removes Emotion from Investment Decisions

Market volatility is uncomfortable. Investors who lack a structured review process tend to react emotionally — panic-selling during downturns or over-concentrating in recent winners.

A scheduled rebalancing plan gives you a pre-decided course of action. Instead of asking “what should I do in this market?”, you follow your plan. This is one of the most underappreciated advantages of portfolio discipline.

4. It Aligns Your Portfolio with Changing Life Goals

Your financial goals at 32 are not the same as at 45. A rebalancing review is also an opportunity to reassess whether your target allocation still fits your current life stage — approaching retirement, funding a child’s education, or building a home purchase corpus.

A Practical Example of Portfolio Rebalancing in India

Let’s walk through a straightforward illustration using Indian rupee figures.

Starting Portfolio (January)

| Asset Class | Amount (₹) | Allocation |

| Equity Mutual Funds | 6,00,000 | 60% |

| Debt Mutual Funds | 4,00,000 | 40% |

| Total | 10,00,000 | 100% |

After 12 Months (Strong Equity Year)

| Asset Class | Amount (₹) | Allocation |

| Equity Mutual Funds | 8,40,000 | 68% |

| Debt Mutual Funds | 4,00,000 | 32% |

| Total | 12,40,000 | 100% |

Your target was 60-40. Your actual portfolio is now 68-32 — meaningfully more aggressive.

Rebalancing Action

Target allocation on ₹12,40,000:

- Equity: 60% = ₹7,44,000

- Debt: 40% = ₹4,96,000

Action required: Redeem ₹96,000 from equity funds and invest it into debt funds.

Result: Your portfolio is back to 60-40 — aligned with your original risk preference.

How Often Should You Rebalance Your Portfolio?

This is one of the most frequently searched questions by Indian investors, and the answer depends on your preferred approach.

Calendar-Based Rebalancing (Recommended for Most Investors)

Review and rebalance your portfolio at fixed intervals — typically every 6 to 12 months. This is the most practical approach because:

- It requires minimal monitoring between reviews

- It avoids over-trading and unnecessary transaction costs

- It keeps you disciplined without becoming obsessive

A simple habit: schedule a portfolio review every April (after the financial year ends) and again in October.

Threshold-Based Rebalancing (For Active Investors)

Some investors prefer to rebalance only when an asset class drifts beyond a predefined band — typically 5% to 10% from the target allocation.

For example, if your equity target is 60%, you only act when it crosses 65% or falls below 55%.

This approach is more responsive but requires ongoing monitoring.

Which Approach Is Right for You?

For most retail investors in India, a calendar-based approach reviewed annually offers the best balance of simplicity, cost-efficiency, and discipline. More active investors or those with larger portfolios may benefit from threshold-based monitoring alongside periodic reviews.

Common Questions About Portfolio Rebalancing

Does rebalancing hurt my returns?

In the short term, it may appear to cap upside — you’re selling winners, after all. But research consistently shows that disciplined rebalancing improves risk-adjusted returns over longer time horizons by preventing excessive concentration in any one asset class.

What are the tax implications of rebalancing mutual funds in India?

This is an important consideration. When you redeem equity mutual fund units held for less than 12 months, short-term capital gains (STCG) tax at 20% applies. Units held beyond 12 months attract long-term capital gains (LTCG) tax at 12.5% above a ₹1.25 lakh annual exemption (as per current rules).

To minimise tax outflow during rebalancing:

- Use fresh SIP contributions to top up underweighted asset classes before redeeming

- Prioritise rebalancing within tax-advantaged accounts where available

- Time redemptions to benefit from long-term capital gains rates

Can SIPs help with rebalancing?

Yes. One practical, low-friction approach is directing new SIP investments toward whichever asset class is currently underweight. This reduces or eliminates the need to sell existing holdings and minimises tax events.

What if I have multiple mutual funds across asset classes?

Consolidation matters. Many investors accumulate too many schemes over time, making allocation tracking difficult. A cleaner portfolio with fewer, well-chosen funds is generally easier to rebalance systematically.

What Makes a Good Portfolio Rebalancing Strategy?

Based on our experience advising clients across different wealth stages, an effective rebalancing strategy shares a few common characteristics:

It is written down. Your target allocation, your review frequency, and your rebalancing thresholds should be documented — not kept in your head.

It accounts for your full financial picture. Rebalancing equity and debt is only part of the equation. Your emergency fund, insurance coverage, and liquidity needs all affect how aggressively you can rebalance.

It separates emotion from execution. The best rebalancing decisions are made against a plan, not in response to recent market headlines.

It is reviewed periodically, not constantly. Checking your portfolio every day creates anxiety and leads to reactive decisions. Scheduled reviews lead to consistent action.

How Clover Capital Supports Your Rebalancing Discipline

At Clover Capital, we work with investors who understand that wealth creation is not about finding the next big stock — it is about building sound systems and following them.

Our advisory process includes:

Goal-Based Financial Planning: We begin by understanding your financial goals, time horizons, and risk tolerance. Your target asset allocation flows directly from this — it is personal, not generic.

Ongoing Portfolio Monitoring: We track allocation drift across your portfolio and flag when rebalancing becomes necessary, so you don’t have to monitor it yourself.

Tax-Efficient Rebalancing: Our team reviews the tax implications of every rebalancing action and helps you sequence redemptions and fresh investments to minimise unnecessary capital gains liability.

Behavioural Guardrails: We help you stay on course during periods of market stress or euphoria — precisely when the temptation to deviate from your plan is strongest.

Comprehensive Review Meetings: Every six months, we sit down with clients to review portfolio performance, reassess life goals, and make allocation decisions with full context.

The Bottom Line on Portfolio Rebalancing

Portfolio rebalancing is one of those investing habits that sounds simple but requires genuine discipline to maintain over years and decades.

The core logic is straightforward: markets will drift your portfolio away from what you originally intended. Left uncorrected, that drift increases your risk exposure and misaligns your investments with your actual goals.

Systematic rebalancing — whether calendar-based, threshold-based, or a combination — restores that alignment. It enforces a buy-low, sell-high discipline that most investors struggle to apply on their own. And it replaces emotionally driven market reactions with a structured, pre-decided plan.

If you would like to understand what your current portfolio’s asset drift looks like, and whether your allocation still matches your goals, our advisers at Clover Capital are available for a no-obligation review.

This article is intended solely for educational and informational purposes and does not constitute investment advice or a solicitation to buy or sell any securities or financial instruments. All investment decisions should be made in consultation with a SEBI-registered investment adviser after assessing your individual financial objectives, risk appetite, and suitability. Past performance is not indicative of future results.

Clover Capital is a [SEBI-registered investment advisory firm / AMFI-registered distributor — please confirm applicable registration]. For personalised advice, please reach out to our advisory team.