Want higher returns without taking unnecessary risks? It starts with asset allocation.

In 2026, smart investors aren’t chasing “hot funds”—they’re building balanced portfolios that grow steadily, survive volatility, and compound wealth over time.

If you get asset allocation right, you won’t need to time the market.

What is Asset Allocation?

Asset allocation is the process of dividing your investments across different asset classes like:

- Equity (growth)

- Debt (stability)

- Gold (hedge)

- International assets (diversification)

Why does it matter?

Because no single asset performs well all the time.

A well-diversified allocation:

- Reduces risk

- Improves consistency

- Protects during market crashes

Why Asset Allocation is Critical in 2026

Markets have changed.

- Global uncertainties are higher

- Interest rates are cyclical

- New sectors (AI, EV, renewables) are booming

Relying on outdated strategies like the 60:40 rule can limit your returns.

Modern investing = Dynamic Allocation + Smart Rebalancing

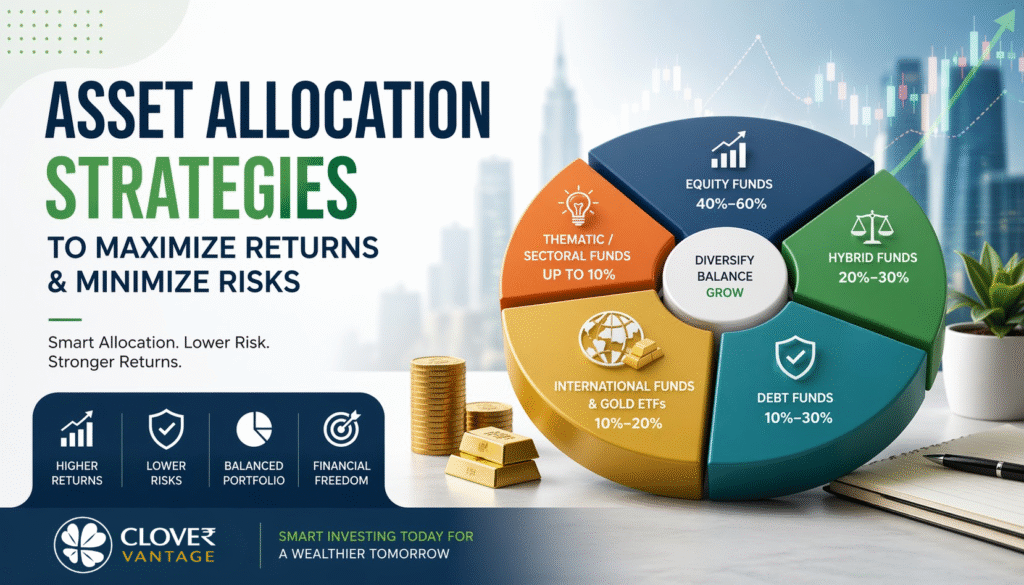

Ideal Asset Allocation Strategy for 2026

Here’s a practical, expert-backed allocation model:

1. Equity Mutual Funds (45%–65%)

Your primary growth engine.

How to allocate:

- Large-cap: Stability

- Mid-cap: Growth

- Small-cap: High return potential

Best for long-term wealth creation (5+ years)

2. Hybrid Funds (15%–25%)

The shock absorbers of your portfolio.

They:

- Balance equity + debt automatically

- Reduce volatility

- Offer smoother returns

Ideal for moderate-risk investors

3. Debt Funds (10%–25%)

Your safety net.

These provide:

- Stable returns

- Liquidity

- Capital protection

Focus on high-quality debt funds in 2026

4. International Funds & Gold ETFs (10%–20%)

This is where most investors go wrong—they ignore global diversification.

Why it matters:

- Exposure to global leaders

- Protection against INR depreciation

- Hedge against inflation

Gold adds stability when markets fall

5. Thematic/Sectoral Funds (Up to 10%)

High-risk, high-reward opportunities.

Trending sectors in 2026:

- Artificial Intelligence

- Electric Vehicles

- Renewable Energy

- Infrastructure

Keep this portion limited to avoid concentration risk.

How Rebalancing Boosts Your Returns

Here’s the truth most investors ignore:

Returns don’t just come from investing—they come from managing your portfolio.

Rebalancing helps you:

- Book profits from overperforming assets

- Reinvest in undervalued areas

- Maintain your risk level

👉 Review your portfolio every 6–12 months

Factor Investing: The Smart Investor’s Edge

In 2026, investors are going beyond traditional funds.

They’re using factor-based investing, focusing on:

- Value stocks (undervalued)

- Momentum stocks (trending upward)

- Quality stocks (strong fundamentals)

- Low volatility stocks (stable performers)

Result? Better risk-adjusted returns.

Tax-Efficient Investing Strategies

It’s not what you earn—it’s what you keep.

Smart investors:

- Use ELSS funds for tax savings (Section 80C)

- Choose direct plans to reduce costs

- Avoid excessive switching (cuts tax + charges)

Lower cost = Higher long-term returns

Common Asset Allocation Mistakes to Avoid

Let’s keep it real—most investors make these mistakes:

Over-investing in equity during bull markets

Ignoring debt and gold

No global exposure

Not rebalancing portfolios

Chasing past returns

Fix this, and your returns will improve automatically.

Example Portfolio (Balanced Investor – 2026)

Here’s a sample allocation:

- Equity Funds: 55%

- Hybrid Funds: 20%

- Debt Funds: 15%

- International + Gold: 10%

This balances growth + stability + diversification

Final Thoughts: Strategy Beats Timing

You don’t need to predict the market.

You need a system that works in every market condition.

That’s exactly what asset allocation does.

When you:

- Diversify properly

- Rebalance regularly

- Stay disciplined

You create a portfolio that grows consistently—without unnecessary stress.

FAQs

1. Is SIP better than lump sum in 2026?

SIP is better for most investors as it reduces market timing risk and builds discipline. Lump sum works well during market corrections.

2. How often should I rebalance my portfolio?

Ideally every 6–12 months, or when allocation deviates significantly.

3. How much should I invest in equity?

Depends on your risk profile, but typically 45%–65% for long-term investors.

4. Are international funds necessary?

Yes. They provide global exposure and reduce dependence on a single economy.

5. Is gold still relevant in 2026?

Absolutely. Gold acts as a hedge during inflation and market volatility.

Ready to Build a Smarter Portfolio?

At Clover Capital, we don’t just recommend funds—we design strategies tailored to your goals, risk profile, and market conditions.

Get expert guidance today and build a portfolio that actually performs.

Pingback: What are investment opportunities for HNI’s in India? - Clover Capital

Pingback: Portfolio Allocation Strategy Using Mutual Funds - Clover Capital