There’s been a surge lately in people treating mutual funds like a guaranteed path to wealth.

“Just do SIP.”

“14–15% returns bro.”

“Compounding will take care of everything.”

That narrative is… incomplete.

This post isn’t anti-mutual funds. It’s anti-oversimplification. Because if you don’t understand what’s happening beneath the surface, you’re not investing—you’re just hoping.

The Typical “Dream Plan” Everyone Quotes

Let’s break down a fairly aggressive (but commonly marketed) scenario:

- Monthly SIP : ₹1,00,000

- Annual step-up: 10%

- Investment duration: 20 years

- Expected returns: 14% (equity mutual funds)

On paper, this gives you a ~₹24–25 crore corpus.

Sounds like financial freedom, right?

Not so fast.

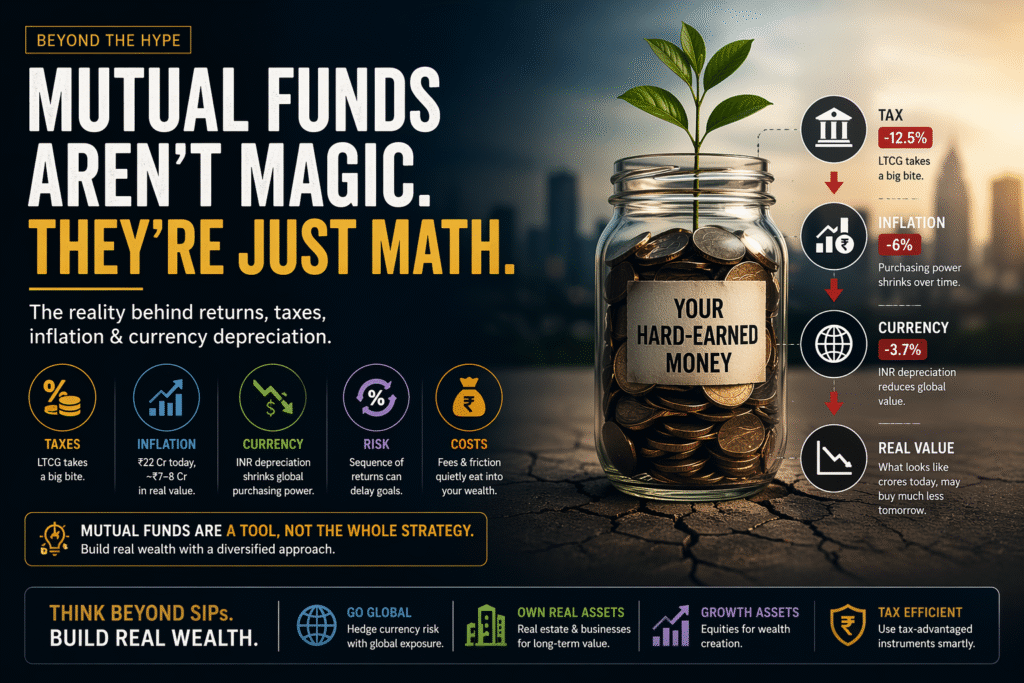

Step 1: The Tax Reality (LTCG is Not Optional)

As of now, long-term capital gains (LTCG) on equity are taxed at 12.5% (above exemption).

So your ₹24.8 Cr isn’t yours.

- Approx tax liability: ~₹2.2 Cr

- Post-tax corpus: ~₹22.5 Cr

That’s your actual number.

And this is assuming tax rules don’t get worse over 20 years (which is optimistic).

Step 2: Inflation — The Silent Wealth Destroyer

India’s long-term inflation hovers around 5–6%.

Let’s assume 6%.

Over 20 years:

- Prices roughly triple

- ₹1 crore in 2046 ≈ ₹31–32 lakh in today’s terms

So your ₹22.5 Cr?

👉 Real purchasing power: ~₹7–8 Cr (today’s value)

This is the biggest illusion in personal finance:

You don’t spend returns. You spend purchasing power.

Step 3: Currency Depreciation — The Global Reality

The INR has historically depreciated ~3–4% annually against USD.

That means:

- Your “14% returns” ≈ ~10% in global terms

- Any global expense (education, travel, imports, even tech) becomes costlier

So your wealth is growing in a weakening currency.

In practical terms:

👉 Your ₹22 Cr doesn’t behave like ₹22 Cr globally

👉 It behaves closer to ₹6–7 Cr in real global purchasing power

Step 4: Sequence of Returns Risk (Nobody Talks About This)

That 14% is an average, not a guarantee.

Reality looks like:

- +20%, -15%, +12%, -10%, +18%…

Now imagine:

Market crashes in Year 18–20

Your retirement or goal is near

You don’t have time to “wait for recovery.”

This is called sequence risk, and it can delay your goals by 5–10 years.

Step 5: Costs & Friction (The Hidden Leak)

Even “low-cost” mutual funds charge:

- Expense ratios: ~0.5% to 2% annually

This seems small—but over 20 years, it can eat 15–25% of your total gains due to compounding.

Also:

- Fund houses earn regardless of your returns

- You bear 100% market risk

So… Are Mutual Funds Bad?

No.

But they are not a complete wealth strategy.

They are:

Great for disciplined investing

Ideal for beginners

Efficient vs traditional savings

Not enough alone for serious wealth creation

What Most People Miss

If your entire plan is:

“SIP in mutual funds = financial freedom”

You’re exposed to:

- Inflation risk

- Currency risk

- Market timing risk

- Policy/taxation risk

That’s not diversification. That’s concentration in one system.

What Actually Builds Real Wealth (Long-Term Thinking)

To go beyond “comfortable” and move toward real wealth, you typically need a mix of:

1. Global Exposure

- US equities / international funds

- Protects against INR depreciation

2. High-Growth Assets

- Equity (direct or funds)

- Business ownership / side income

3. Hard Assets

- Real estate (selectively)

- Acts as partial inflation hedge

4. Tax-Efficient Instruments

- PPF / VPF / EPF (limited but powerful)

The Real Verdict

Mutual funds are:

A tool, not a strategy

A foundation, not the full building

They help you participate in growth

But they don’t guarantee financial independence

Final Thought

If you rely only on mutual funds, you may still reach your goals.

But:

- Your “crores” may not feel like crores

- Your timeline may stretch longer than expected

- Your lifestyle expectations may need adjustment

So invest in MFs—but also invest in understanding money itself.

Because the biggest risk isn’t the market.

It’s believing a simplified story about it.