If you’re investing in mutual funds but ignoring taxation, you’re only seeing half the picture.

In 2026, mutual fund taxation in India has evolved—and understanding it can directly impact your real returns.

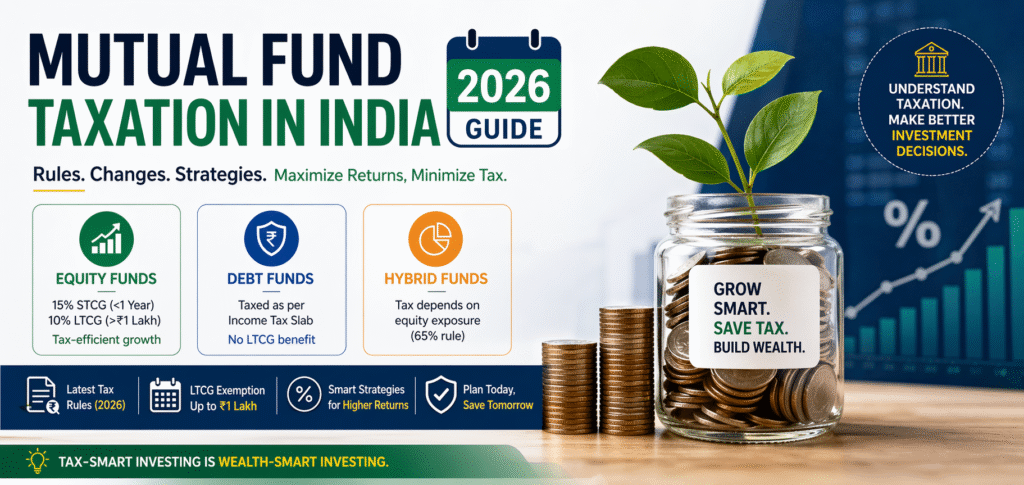

This guide breaks down how regular equity funds, debt funds, and hybrid funds are taxed—simply, clearly, and in a way that actually helps you make better investment decisions.

What is Mutual Fund Taxation?

Mutual fund taxation refers to the tax you pay on the profits (capital gains) earned from your investments.

These gains are classified into:

- Short-Term Capital Gains (STCG)

- Long-Term Capital Gains (LTCG)

The taxation depends on:

- Type of fund (Equity / Debt / Hybrid)

- Holding period

- Recent tax rules under Indian law

Tax Rules You Must Know (2026 Update)

Recent updates have changed how different mutual funds are taxed, especially debt and hybrid categories.

Taxation is governed under:

- Income Tax Act 1961

- Capital gains rules applicable to financial assets

1. Tax on Regular Equity Funds

These funds invest 65% or more in equities.

Tax Structure:

- STCG (held < 1 year)

Taxed at 15% - LTCG (held > 1 year)

Gains up to ₹1 lakh: Tax-free

Gains above ₹1 lakh: 10% tax

Example:

If you earn ₹2 lakh profit after 1 year:

- ₹1 lakh = No tax

- ₹1 lakh = 10% → ₹10,000 tax

2. Tax on Debt Funds (Major Change)

Debt funds invest in bonds, government securities, etc.

New Rule (Post-2023 Update):

- No LTCG benefit anymore

- No indexation benefit

Tax Structure:

- All gains are taxed as per your income tax slab

Whether you hold for 1 year or 5 years—same taxation applies

What This Means:

- If you’re in the 30% bracket → you pay 30% tax

- Debt funds are now similar to FD taxation

3. Tax on Hybrid Funds

Hybrid funds invest in a mix of equity and debt.

Tax depends on equity exposure:

If Equity ≥ 65%:

- Taxed like equity funds

If Equity < 65%:

- Taxed like debt funds (slab rate)

Quick Comparison Table

| Fund Type | Short-Term Tax | Long-Term Tax | Key Benefit |

| Equity Funds | 15% (<1 year) | 10% (>₹1L) | Tax-efficient growth |

| Debt Funds | Slab rate | Slab rate | Stable but tax-heavy |

| Hybrid Funds | Depends | Depends | Flexibility |

Common Mistakes Investors Make

- Ignoring tax while choosing funds

- Holding debt funds expecting old indexation benefits

- Selling equity funds before 1 year (higher tax)

- Not planning withdrawals strategically

Smart Tax-Saving Tips

- Hold equity funds for more than 1 year

- Use ₹1 lakh LTCG exemption smartly every year

- Choose hybrid funds wisely based on tax impact

- Combine ELSS (for tax saving) + equity funds (for growth)

FAQ Section

1. Is SIP taxed differently than lump sum?

No. Tax depends on the holding period of each SIP installment, not the method.

2. Are debt funds still better than FDs?

From a tax perspective—they are now similar. But debt funds still offer better liquidity and flexibility.

3. How to legally reduce tax on mutual funds?

- Use LTCG exemption

- Invest in ELSS under Section 80C of Income Tax Act

- Plan withdrawals across financial years

4. Which mutual fund is most tax-efficient?

Equity funds and ELSS are currently the most tax-efficient options in India.

Final Takeaway

Mutual fund taxation in India 2026 is not complicated—but it is critical.

- Equity funds → Best for tax-efficient growth

- Debt funds → Safer but higher tax impact

- Hybrid funds → Flexible, but depends on allocation

The smartest investors don’t just chase returns—they optimize taxes too.