By Prasenjit Gupta, Founder, Clover Capital | Wealth Management & Financial Services, Kolkata.

AMFI-registered Mutual Fund Distributor | 55+ man-years of combined advisory experience.

Published: May 2026 | Last reviewed: May 2026.

Quick answer: If you want one fund to own and forget, Flexi Cap. If you want mandatory diversification across all market sizes, Multi Cap. If you want the growth potential of mid-caps with the stability of large-caps, Large & Mid Cap. But the real answer depends on your goals, your risk tolerance, and how many funds you own. This guide will walk you through it.

Most investors pick mutual funds by looking at last year’s returns. That is exactly the wrong way to do it.

Before you compare past performance, understand what each fund can do.

SEBI’s categorisation rules define a fund’s basic nature. A Flexi Cap fund and a Multi Cap fund can both hold stocks across large, mid, and small companies. But they operate under entirely different mandates, take different risks, and behave differently in a falling market.

If you don’t understand the category, you can’t evaluate the fund.

In this guide, we break down three of the most popular — and most confused — equity mutual fund categories: Flexi Cap, Multi Cap, and Large & Mid Cap. We’ll explain what SEBI requires of each, how they actually behave, who each is suited for, and how to decide which belongs in your portfolio.

A Quick Primer: Why SEBI Created These Categories

Until 2017, Indian mutual funds were a naming chaos. An AMC could call a fund anything—”Opportunities Fund,” “Advantage Fund,” or “Growth Fund.” Those names may not say where the money was invested. Many so-called large-cap funds quietly held significant mid and small-cap positions. Investors couldn’t compare apples to apples.

SEBI’s landmark circular from October 2017 on categorizing and rationalizing mutual fund schemes changed this permanently. SEBI:

- Defined exactly what Large Cap, Mid Cap, and Small Cap mean (by market capitalisation rank)

- Required each AMC to offer only one scheme per category

- Mandated minimum and maximum allocation percentages for each category

- Required fund names to match their category mandates

Then in September 2020, SEBI tightened Multi Cap rules — and in November 2020, created the Flexi Cap category in response. Most recently, the February 2026 SEBI circular raised minimum equity exposure requirements further for several categories, reinforcing the “true-to-label” principle.

The result: today’s fund categories are meaningful. The category tells you what the fund must do with your money, regardless of which AMC runs it.

First, Let’s Define the Market Cap Tiers

Every discussion of these three categories rests on SEBI’s definition of market capitalization bands (based on AMFI’s semi-annual ranking):

| Tier | Definition | Examples (as of 2025–26) |

| Large Cap | 1st to 100th company by market cap | Reliance, TCS, HDFC Bank, Infosys, ICICI Bank |

| Mid Cap | 101st to 250th company by market cap | Trent, Coforge, Persistent Systems, Tube Investments |

| Small Cap | 251st company onwards | 251st company onwards |

SEBI requires AMCs to rebalance their portfolios semi-annually against the AMFI list. This matters because companies can move between tiers. A mid-cap that grows a lot can become large-cap. Funds must respond to these changes.

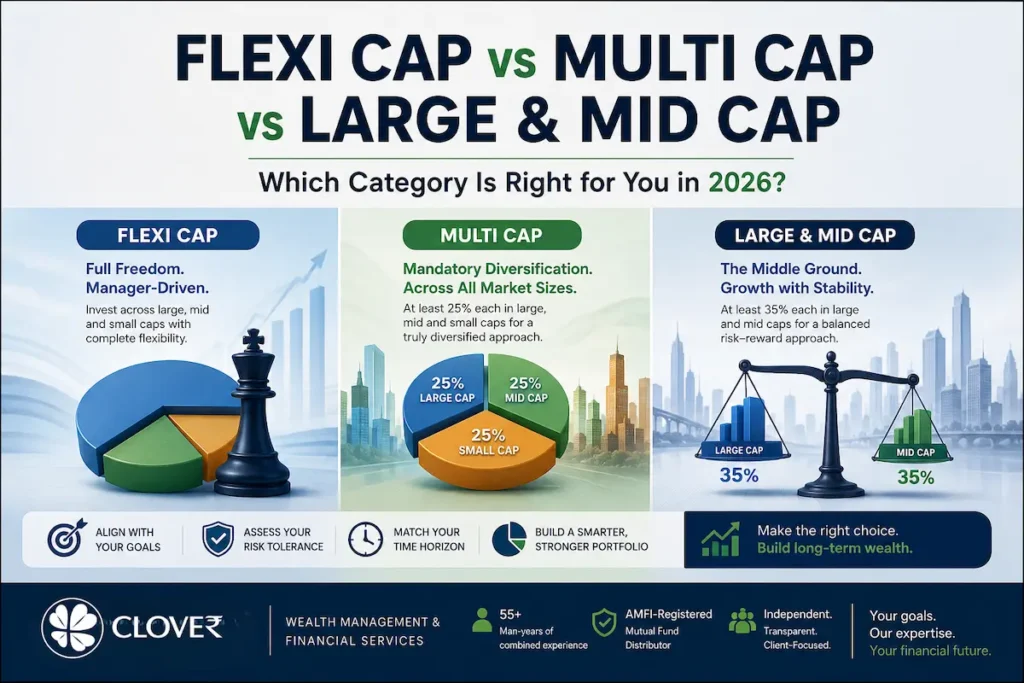

Flexi Cap Funds: Full Freedom, Manager-Driven

What SEBI Requires

A Flexi Cap fund must invest at least 65% of assets in equity and equity-related instruments. Beyond that minimum, there is no restriction on how much goes into large, mid, or small caps. The fund manager can put 80% in large caps today and shift 40% to mid-caps next quarter — entirely at their discretion.

Regulatory basis: SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2020/228, November 6, 2020

What This Means in Practice

Flexi Cap is, in essence, the fund manager’s canvas. The fund manager’s judgment — their reading of market cycles, sector rotations, and valuations — determines where your money sits at any given time.

When markets are expensive (high P/E ratios across the board), a good Flexi Cap manager shifts toward large caps or even raises cash. When mid and small caps offer value after a correction, they rotate aggressively into those segments.

This is why Flexi Cap performance varies enormously between funds. It’s not just about market returns — it’s about how skillfully the manager navigates the freedom SEBI has given them.

In practice, most Flexi Cap funds today carry a large-cap bias — typically 50–70% in the top 100 companies — because that’s where experienced managers find the most liquidity and risk-adjusted opportunity. But this is not mandated. Some Flexi Caps, like Quant Flexi Cap, have historically swung aggressively into small caps during rally phases.

5-Year Performance Context

According to AMFI data, as of December 2025, Flexi Cap funds delivered average 5-year returns of 18–27% CAGR.

The top performers delivered over 25% annualised returns. The category is one of the most actively managed in Indian mutual funds.

Returns vary widely between the best and worst funds.

This highlights the importance of choosing the right fund in this category.

Who Should Invest in Flexi Cap

Flexi Cap suits you if:

- You want a single, diversified equity fund and prefer not to manage multiple funds

- You trust an experienced fund manager’s judgment to navigate different market conditions

- You have a 7-year or longer investment horizon

- You have moderate to high risk tolerance — returns can be volatile, especially if the manager has mid/small-cap tilt

- You’re a first-time equity investor building their first serious mutual fund portfolio

Flexi Cap’s One Honest Risk

Because there are no mandatory allocation floors, a Flexi Cap manager can keep the portfolio heavy in large caps. Some managers do this even when mid- and small-cap opportunities exist. This can lead to a fund that acts like a large-cap fund. You may still pay the higher expense ratio of a “diversified equity” fund. Always check a Flexi Cap’s actual portfolio allocation before investing.

Multi-Cap Funds: Mandated Diversification Across All Three Tiers

What SEBI Requires

Multi Cap funds must invest at least 25% in large caps, 25% in mid caps, and 25% in small caps. At least 75% must be in equity. This is SEBI’s hardest allocation rule in the equity category.

Regulatory basis: SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2020/221, September 11, 2020

This rule was introduced after SEBI noticed that multi-cap funds acted like large-cap funds. Most of the portfolio was in the Nifty 50. There was little exposure to mid or small-cap stocks. SEBI essentially said: if you call yourself multi-cap, you must be diversified across all sizes.

What This Means in Practice

The 25-25-25 minimum rule means that at all times, at least a quarter of your money is in mid caps and at least a quarter is in small caps. This is a fundamentally different risk profile from a Flexi Cap that has freedom to go conservative.

In a bull market: Mandatory small- and mid-cap exposure is a strong tailwind. Mid and small caps often outperform large caps in sustained rallies.

In a bear market or correction: The mandatory exposure to smaller companies is a headwind. Small caps can fall 40–50% in sharp corrections, and Multi Cap funds cannot reduce this exposure below 25% even if the manager wants to. Understanding how to invest during periods of market uncertainty is equally important.

This means Multi Cap funds are structurally more volatile than Flexi Cap funds that maintain large-cap bias. The trade-off: higher potential returns over long cycles, higher drawdowns during corrections.

Who Should Invest in Multi Cap

Multi Cap suits you if:

- You want guaranteed exposure to mid and small caps without managing three separate funds

- You believe in the long-term wealth creation potential of smaller Indian companies

- You have a 10-year or longer investment horizon — enough time to ride out small-cap drawdowns

- You have high risk tolerance and can stomach a 30–40% portfolio drawdown without selling

- You’re an experienced investor who understands the risk-return profile of mid and small caps

- You want systematic, rules-based diversification rather than depending on a manager’s discretion

The Multi Cap Honest Caveat

The mandatory 25% small-cap floor is the category’s double edge. Some of the best small-cap opportunities come after significant corrections — when valuations are cheap and recovery potential is high.

A Multi Cap manager must maintain that 25% floor even when small caps are overvalued, which can drag returns. Conversely, they can’t reduce small-cap exposure to protect the portfolio during crashes. This removes an important risk-management tool.

Large & Mid Cap Funds: The Middle Ground

What SEBI Requires

Large & Mid Cap funds must invest at least 35% in large-cap stocks. They must also invest at least 35% in mid-cap stocks. Together, these must total at least 80% in equities. This rule was updated under the February 2026 SEBI circular.

Regulatory basis: SEBI Circular October 6, 2017, updated February 26, 2026

The remaining 30% of the portfolio can be allocated at the fund manager’s discretion — to large caps, mid caps, or even small caps.

What This Means in Practice

Large & Mid Cap is the fund category designed for investors who want more growth potential than a pure large-cap fund but less volatility than a pure mid-cap fund. The mandatory large-cap floor of 35% provides stability and liquidity; the mandatory mid-cap floor of 35% adds growth potential that a large-cap fund lacks.

In practice, most Large & Mid Cap funds carry 40–50% in large caps, 40–45% in mid caps, and a small balance in other instruments. This makes their risk-return profile sit clearly between Nifty 50 index funds (pure large cap) and mid-cap funds.

Historically, this category has beaten pure large-cap funds over 7–10 years. It has also had smaller drawdowns than pure mid-cap funds. It’s a genuine middle path that doesn’t require you to take a strong view on market cycles.

Who Should Invest in Large & Mid Cap

Large & Mid Cap suits you if:

- You want more upside than a large-cap or index fund but find pure mid-cap funds too volatile

- You’re a wealth builder at the accumulation stage — typically between 30 and 50 years of age

- You have a 7–10 year investment horizon

- You have moderate to high risk tolerance — you can handle drawdowns but prefer the ballast of large-cap stocks

- You want predictable diversification across two major market segments without worrying about small-cap risk

- You already have a large-cap index fund and want to add a growth layer without going all-in on mid caps

The Head-to-Head Comparison:

| Parameter | Flexi Cap | Multi Cap | Large & Mid Cap |

| Large cap minimum | None | 25% | 35% |

| Mid cap minimum | None | 25% | 35% |

| Small cap minimum | None | 25% | None |

| Total equity minimum | 65% | 75% | 80% |

| Who controls allocation? | Fund manager | SEBI rules + fund manager | SEBI rules + fund manager |

| Volatility | Low to High (manager-dependent) | High | Moderate to High |

| Potential return (long-term) | Moderate to High | High | Moderate to High |

| Ideal holding period | 7+ years | 10+ years | 7–10 years |

| Manager skill dependence | Very High | Moderate | Moderate |

| Small-cap exposure | Optional | Mandatory (min 25%) | Minimal/Optional |

| Best market for this category | Any (manager adapts) | Bull markets / long cycles | Steady growth markets |

| Regulatory reference | SEBI Nov 2020 circular | SEBI Sep 2020 circular | SEBI Oct 2017 circular |

A Common Mistake: Holding All Three Together

Many investors who’ve done some research end up holding a Flexi Cap, a Multi Cap, and a Large & Mid Cap fund simultaneously — thinking they’re diversifying. In most cases, they’re not.

Because all three categories can hold the same large and mid-cap companies, portfolio overlap between these funds can be significant. You may get heavy exposure to the same 20 to 30 stocks in three “different” funds. You may pay three separate expense ratios and face more tax complexity across three portfolios. Yet you may not reduce risk.

What to do instead:

If you want broad equity diversification with one or two funds, a well-chosen Flexi Cap or a Large & Mid Cap is usually sufficient. Add a Multi Cap only if you consciously want that mandatory small-cap exposure and are prepared for the associated volatility.

How to Choose: A Practical Decision Framework

Answer these three questions:

1. How long can you stay invested without touching this money?

- Less than 7 years → Large & Mid Cap or Flexi Cap with large-cap bias

- 7–10 years → Flexi Cap or Large & Mid Cap

- 10+ years → Multi Cap becomes genuinely appropriate; the volatility is surmountable over this horizon

2. How comfortable are you with drawdowns?

- “I’ll panic if my portfolio falls 30%” → Flexi Cap with large-cap bias, or large-cap index + small Flexi Cap

- “I can hold through a 30–35% fall” → Large & Mid Cap

- “I can hold through a 40–50% correction without selling.” → Multi Cap is appropriate

3. How many equity funds do you already hold?

- 0–1 equity funds → Flexi Cap as your core holding

- 2–3 equity funds → Check overlap before adding another cross-cap category

- 4+ equity funds → You likely don’t need another multi-cap category fund; consider simplifying

Frequently Asked Questions

What is a Large and Mid Cap Fund?

A Large & Mid Cap Fund is a type of mutual fund that invests in both large-cap and mid-cap companies. According to AMFI guidelines, these funds must invest at least 35% in large-cap stocks and 35% in mid-cap stocks.

- Large-cap companies are well-established businesses with strong market presence and relatively stable performance.

- Mid-cap companies are growing companies that offer higher growth potential but may come with slightly higher risk.

This category aims to provide a balance between:

- Stability from large-cap stocks

- Growth opportunities from mid-cap stocks

Large & Mid Cap Funds suit investors who want more growth than large-cap funds. They still offer some stability in a portfolio. They are generally ideal for long-term goals such as wealth creation, retirement planning, or children’s education.

What are the benefits of investing in Large & Mid Cap Mutual Funds?

Large & Mid Cap Mutual Funds offer a balanced mix of stability and growth. Large-cap stocks usually have lower risk and steady results. Mid-cap stocks often offer higher long-term growth.

This combination helps investors benefit from wealth creation opportunities without taking excessive risk. They are suitable for investors with a medium to long-term investment horizon looking for both growth and diversification.

How do I choose the best Large & Mid Cap Fund?

Choose a fund with a strong long-term track record. Look for steady results across market cycles. Pick funds with experienced managers. Make sure the expense ratio is reasonable.

Also check whether the fund’s portfolio is well-diversified across sectors and companies. Compare returns with its benchmark and peers over 3, 5, and 7 years instead of focusing only on short-term performance.

Can I hold both a Flexi Cap and a Large & Mid Cap fund?

Yes, but check the portfolio overlap first. Many investors find these two categories overlap significantly in their top holdings. If overlap is above 50–60%, you’re largely duplicating, not diversifying.

Is Multi Cap better than Flexi Cap for long-term wealth creation?

Not categorically. Multi Cap offers mandatory small-cap exposure, which has historically contributed to higher long-term returns — but with higher volatility and deeper drawdowns.

Over 10+ year periods, Multi Cap has sometimes outperformed Flexi Cap, but not consistently. It depends heavily on market cycles.

How often do fund categories change?

SEBI periodically issues updated circulars on fund categorisation. The most recent significant update was February 2026. Always verify current rules on SEBI’s official website (sebi.gov.in) or AMFI (amfiindia.com).

What is the minimum investment?

Most funds in all three categories accept SIP investments starting from ₹500–₹1,000 per month. There is no SEBI-mandated minimum for retail investors.

The Bottom Line

Flexi Cap, Multi Cap, and Large & Mid Cap are not three versions of the same thing. They reflect three genuinely different philosophies of equity investing:

- Flexi Cap says: trust the manager to decide where to invest. Best when you have a talented fund manager and a long runway.

- Multi Cap says: diversify by rule, not by discretion. Best when you want mandatory all-market exposure and have a decade or more.

- Large & Mid Cap says: the growth layer without going all-in on risk. Best for the wealth-building phase with a 7–10 year view.

Most investors are well-served by one of the first two. Very few need all three.

If you’re unsure which category — or which specific fund — belongs in your portfolio, the answer isn’t a Google search or a Reddit thread. Speak with a professional wealth management advisor.

Speak with Clover Capital

At Clover Capital, we build equity portfolios based on your goals, time horizon, and risk tolerance. We do not base them on industry trends or commission structures. As an independent, product-agnostic advisory firm, our only mandate is what’s right for you.

We work with HNIs, NRIs, young professionals, and business families across India.

📍 Kolkata Office: Constantia Building, 8th Floor, Wing B, 11 Dr. U N Brahmachari Road, Kolkata – 700017 📞 +91 9147047488 ✉️ hello@clovercapital.in 🌐 clovercapital.in

Disclaimer: This article is for educational and informational purposes only. It does not constitute investment advice. Mutual fund investments are subject to market risks. Past performance is not indicative of future returns. Please read all scheme-related documents carefully before investing. Readers are advised to consult a SEBI-registered investment advisor before making any investment decisions. Clover Capital is an AMFI-registered Mutual Fund Distributor.

Regulatory references: SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2017/114 (October 6, 2017); SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2020/221 (September 11, 2020); SEBI Circular SEBI/HO/IMD/DF3/CIR/P/2020/228 (November 6, 2020); SEBI Circular February 26, 2026. Data references: AMFI (amfiindia.com); Value Research (valueresearchonline.com).

Last updated: May 2026